📊 Comparison Table: XIRR vs CAGR vs IRR vs Absolute Return

| Parameter | XIRR | CAGR | IRR | Absolute Return |

|---|---|---|---|---|

| Meaning | Annualized return for irregular cash flows | Annual growth rate for a lump-sum investment | Annualized return for regular cash flows | Total return without considering time |

| Best Used For | SIPs, top-ups, irregular investments | Lump-sum investments | Projects or investments with periodic cash flows | Short-term or simple comparisons |

| Considers Dates? | ✔ Yes | ✔ Yes (only start & end) | ✔ Yes (for each cash flow) | ❌ No |

| Suitable For SIPs? | ✔ Best option | ❌ Not accurate | ❌ Usually not used for SIPs | ❌ Not suitable |

| Cash Flow Flexibility | High — works with any amount/date | Low — requires single lump-sum | Medium — works only with regular flows | None — ignores timing |

| Formula Complexity | High (requires software or Excel) | Low (simple formula) | High (Iteration formula) | Very Low (basic math) |

| Shows Real Return? | ✔ Very Accurate | ✔ Accurate (for lump-sum) | ✔ Accurate (for regular flows) | ❌ Not accurate over long periods |

| Used By | Mutual funds, advisors, SIP reports | AMCs for lump-sum fund performance | Corporate finance, capital projects | Beginners, short-term trackers |

| Time Value of Money? | ✔ Yes | ✔ Yes | ✔ Yes | ❌ No |

| Interpretation | Actual annual return after factoring every cash flow date | Average annual return | Annual return where NPV = 0 | Simple percentage gain or loss |

What Is XIRR and Why Do Most Investors Trust It to Measure Real Returns?

XIRR (Extended Internal Rate of Return) is a method used to calculate the actual return you earn from a mutual fund when your investments happen at different times and in different amounts — like SIPs, lumpsum additions, or withdrawals.

Unlike simple return calculations, XIRR considers two things:

- Every cash flow (each SIP installment, top-up, or partial withdrawal)

- The exact date on which the money moved in or out

Because each investment amount stays invested for a different number of days, XIRR gives a more accurate picture of your real profit.

In simple words:

XIRR tells you the true annual return you earned on your mutual fund by tracking when and how much you invested. It’s the best way to know how your SIPs or irregular investments actually performed.

Why XIRR matters:

- Gives a realistic return percentage

- Works for SIPs, lump sums, and mixed transactions

- Helps compare funds fairly

- Better than CAGR (Compound Annual Growth Rate) when multiple investments are made over time

Example (simple):

If you invest monthly through SIPs, each installment grows for a different period. XIRR calculates a single yearly return that combines all these varied durations correctly.

What Exactly Is XIRR in Mutual Funds and Why Is It the Most Accurate Way to Measure Your Returns?”

XIRR (Extended Internal Rate of Return) Since, SIPs and irregular investments don’t happen on the same date or with the same amount, XIRR helps you find one single annual return that reflects all those cash flows correctly.

In simple words:

XIRR tells you how much your money actually grew per year, considering:

Why XIRR is used:

- SIPs involve monthly payments, not one-time investment

- Each installment stays invested for a different number of days

- Simple returns or CAGR cannot show the accurate picture

- XIRR gives the most realistic performance number for mutual funds

Example (very simple):

If you invest ₹5,000 every month, XIRR checks the date of each payment and calculates how much return those payments generated till today. It then gives one annual return percentage.

Is XIRR Really the Most Accurate Way to Track Your SIP Returns?

XIRR is the most accurate way to measure how your SIP has genuinely performed.

Because every SIP installment is invested on a different date—and under different market conditions—each payment gets a different amount of time to grow. XIRR captures this by considering every single cash flow along with its exact date, and then calculating one true annualized return for the entire investment.

Put simply, XIRR reveals the real growth rate of your SIP, not just an average figure. It tracks how and when your money went into the fund and how long each installment stayed invested, making it far more reliable than basic return methods.

How Is XIRR Calculated in Mutual Funds, and Why Do Investors Trust It for Real Return Measurement?

XIRR is calculateXIRR calculates your return by considering every investment amount, every investment date, and your final portfolio value, and then finding one annual return rate that makes all these cash flows balance out to zero. This is why it reflects the real performance of your SIP or staggered investments.

How It Works (Step-by-Step Explanation)

- You invest different amounts on different dates (SIPs, lump-sum deposits, top-ups).

- Each investment stays in the market for a different period of time.

- XIRR takes all these cash flows and figures out one single annual return that explains how your total investment grew to today’s value.

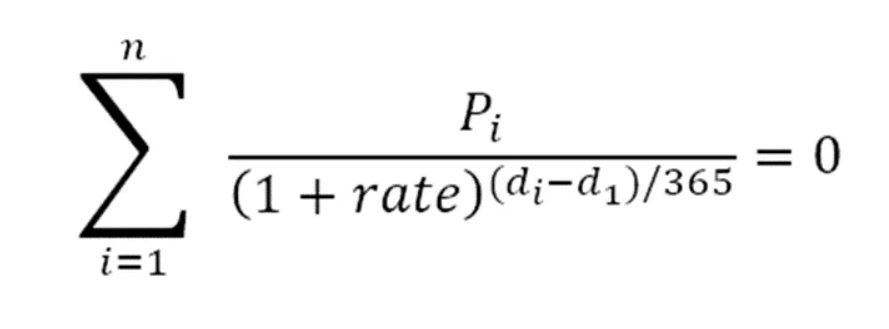

What the XIRR Formula Tries to Do

XIRR solves for a return rate “r” such that:

Present value of all your investments = Present value of your final fund value

Because every cash flow happens on a different date, the formula adjusts for:

- how long each investment stayed invested

- the return required to reach today’s value

This is why XIRR is the most realistic return metric for SIPs, step-up SIPs, and irregular investments.

Easy Example

Suppose you invest:

- ₹5,000 in January

- ₹5,000 in February

- ₹5,000 in March

And today your mutual fund value is ₹18,000.

XIRR works backward to find the annual return rate that connects all your investments to today’s final amount.

That single percentage is your XIRR.

Capitalment Important Point

You don’t calculate XIRR manually because the formula requires trial-and-error numerical solutions.

Instead, XIRR is automatically calculated by:

- Excel / Google Sheets (using the XIRR function)

- Mutual fund apps

- Portfolio trackers

- AMC statements

These tools handle all date-based cash flow adjustments for you.

What Is the XIRR Formula and Why Do Investors Trust It for Calculating Real Returns?

The XIRR formula is used to calculate the rate of return when money is invested or withdrawn on different dates. Since every cash flow happens at a different time, the formula adjusts the return based on actual dates.

XIRR Formula:

Meaning of the terms:

- di is the last payment date.

- d1 is the 0th payment date.

- Pi is the last payment.

The goal of the formula is to find r (your real return) that makes the total present value of all cash flows equal to zero.

In Simple Words:

XIRR tries different return values (r) until it finds the one that balances all your investments and withdrawals when adjusted for the exact number of days.

Key Point:

You don’t calculate XIRR manually. Tools like Excel, Google Sheets, and mutual fund apps use this formula behind the scenes.

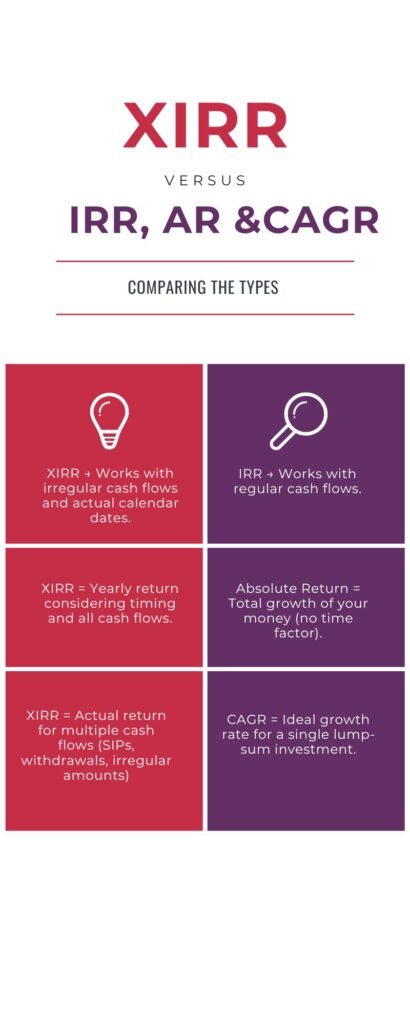

XIRR vs IRR

XIRR (Extended Internal Rate of Return)

XIRR is a more flexible version of IRR. It calculates return when money goes in and out on irregular dates—which is how most real-life investments actually work.

It is used for SIPs, mutual funds, and any investment where the cash flow dates are not evenly spaced.

IRR (Internal Rate of Return)

IRR tells you the return on an investment assuming the cash flows come at regular intervals—for example, yearly or monthly.

It works well when money is invested and received in a fixed pattern.

Key Difference (Very Short)

- IRR → Works with regular cash flows.

- XIRR → Works with irregular cash flows and actual calendar dates.

XIRR vs CAGR (In Simple, Original Words)

XIRR (Extended Internal Rate of Return)

- XIRR shows the actual return you earned, considering every deposit and withdrawal made at different dates.

- It captures real-life cash flows, so it’s more accurate for SIPs, top-ups, or irregular investments.

- Use this when you invest multiple times or on different dates.

CAGR (Compound Annual Growth Rate)

- CAGR shows the average yearly growth rate of your investment when money is invested once and stays untouched.

- It assumes your investment grows smoothly every year, even though real markets fluctuate.

- Use this when you invest a lump sum.

Quick Difference (One Line Each)

- CAGR = Ideal growth rate for a single lump-sum investment.

- XIRR = Actual return for multiple cash flows (SIPs, withdrawals, irregular amounts).

XIRR vs Absolute Return (In Simple Words)

XIRR (Extended Internal Rate of Return)

- XIRR tells you the annualised return considering every cash flow—your SIP deposits, top-ups, partial withdrawals, and redemption.

- It adjusts returns based on dates, making it more accurate for SIPs and irregular investments.

Absolute Return

- Absolute return tells you how much your investment grew in total, from the day you invested to the day you exited.

- It does not consider timing, multiple deposits, or withdrawals.

- Formula:

Absolute Return = (Final Value – Initial Investment) / Initial Investment × 100

Use it when:

You invest one lump sum and hold it for the entire period.

Use it when:

You invest multiple times or at different dates.

In Short

- Absolute Return = Total growth of your money (no time factor).

- XIRR = Yearly return considering timing and all cash flows.

What Does Negative XIRR Mean?

Negative XIRR means your investment has generated a loss overall.

In simple words: The money you got back is less than the money you invested.

So the return rate needed to match your cash flows becomes negative.

Short Example

Imagine you invest ₹10,000 in a mutual fund.

After one year, its value falls and you withdraw ₹9,000.

- Money invested: ₹10,000

- Money received: ₹9,000

- Loss = ₹1,000

Here your XIRR will be negative because the ending amount is lower than what you put in.

One-Line Summary

Negative XIRR = overall loss on your investment.

Example of XIRR:

Invest ₹5,000 on Jan 1

₹5,000 on Feb 1

₹5,000 on Mar 1

Redeem ₹16,500 on Dec 1

👉 XIRR gives the true annual return considering all dates.

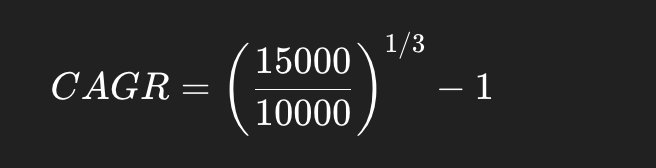

Example of CAGR:

Invest ₹10,000 → grows to ₹15,000 in 3 years

Example of Absolute Return:

Invest ₹10,000 → becomes ₹12,000

Return = 20%